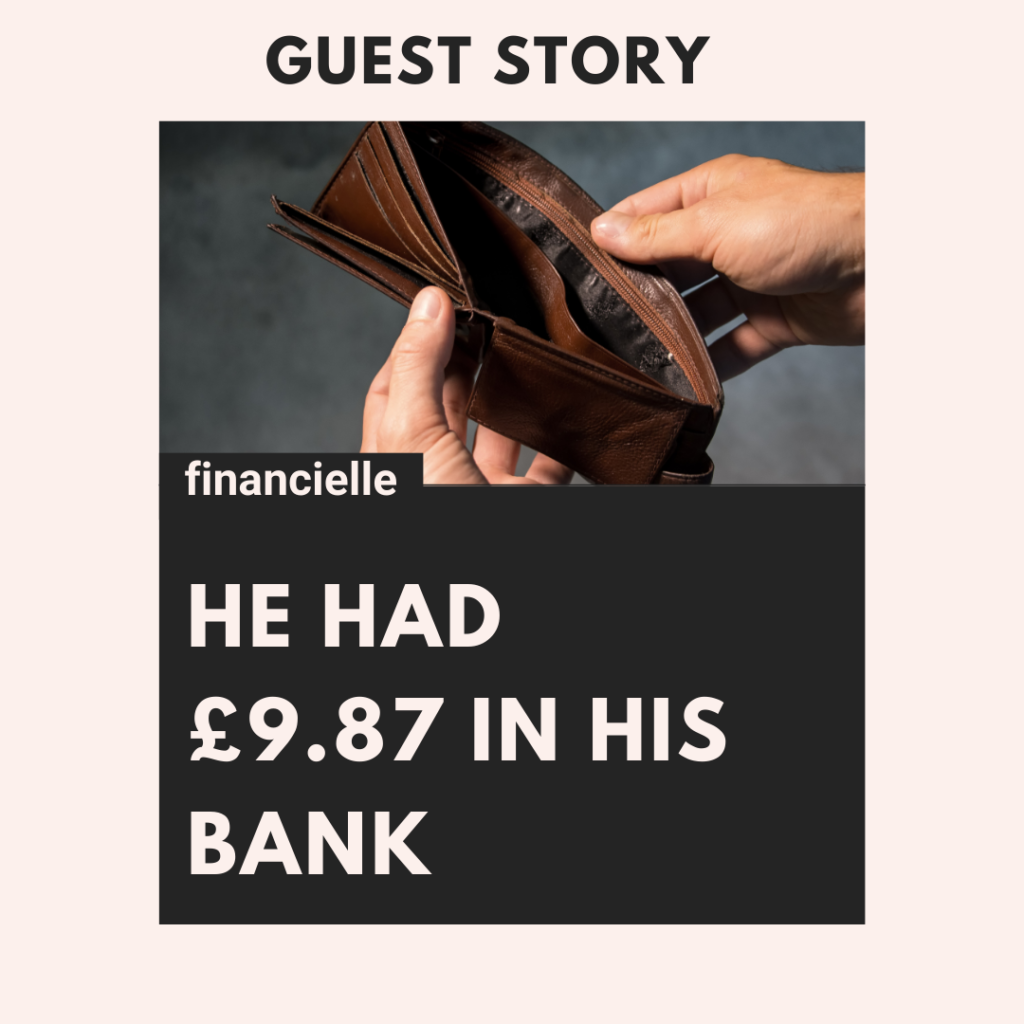

Guest Post: He had £9.87 in his bank account.

This guest blog, we have an incredible community member shared her experience of the aftermath of her Dad’s passing. Her story is emotional, compelling and intended to reinforce the need for us to work on our financial wellbeing not just for us, but also for our families. Your financial wellness will have an impact long after you’re gone, not only as part of your legacy and any assets you leave behind, but also by providing sufficient funds for your family to provide an appropriate funeral.

My dad passed away unexpectedly last August. Something neither of us spoke about often enough were his finances. Dad was an alcoholic so made it difficult to discuss certain subjects with him. He went through chemotherapy for lung cancer 5 years ago and because of this, he set up a funeral plan.

The Finances

After Dad passed away, it became clear very quickly that he had a lot of debt, including:

- numerous high value debts with companies such as Studio and Bright House.

- Over £10,000 in benefits – the DWP wrote to ask me to pay it back out of Dad’s estate

- Hundreds of pounds to doorstep loan companies such as Provident and Shop A Check.

His private pension with Scottish Widows was worth nothing, he had chosen to take a lump sum out meaning that the remainder of his pension fund essentially died with him.

I spoke to the company who he has his funeral plan with, he had taken out a 10 year plan and had only paid into this for 5 years meaning that they would not pay out anything towards the cost.

After waiting for the death certificate we were then able to access his bank. He had £9.87 in his bank.

The Funeral

My brother and I were given details of charities that support with funeral costs for loved ones, however as we both work full time and do not claim any benefits we could not have any help.

The funeral directors advised that they could organise a council funeral but that would mean taking dad to be cremated, no service, no funeral home – ultimately meaning no celebration for Dad’s life.

The cost of the funeral was just over £3,500. It was awful and so sad to have to pick the cheapest of everything such as the coffin, flowers and we chose not to have funeral cars to save on the end cost. This was something my brother and I had not planned for so didn’t have the cash available in one sum to pay.

We had to set up payment plans, the funeral home were absolutely great and we are still paying monthly installments now.

The Aftermath

Dad died on the Saturday and on top of the worry of paying for his funeral, I was also told that as my dad lived in a council property, I would now be liable for his rent from the Monday morning for as long as it took me to clear the flat out – the flat had to be empty or I would face being given a bill from the council to have it cleared. This saw me spend every day for 8 days sometimes 10 hours a day clearing out the flat meaning I didn’t give myself time to process his death, this had and still does have a huge impact on my mental health.

As his next of kin, I still receive solicitor letters, threat of debt collectors and creditors asking for payments which some days I can deal with and other days I find really hard on my own mental health.

Even though we are 8 months on from my Dad’s death, the financial side is still very much a daily thought process for me.

By bravely sharing her story, we hope that this helps to give you a fresh perspective on the wider reasons to work to be financially well. We’re also so very proud of her and her brother for doing what they could in their Dad’s memory.

Click to read the blog post You Need To Do A Will Now.

Mum’s get 17 minutes a day…

Did you know that, on average, Mum’s get seventeen minutes to themselves every day? I don’t know about you but I think that seems generous… Whether you are a parent or not, self care is often something most people neglect when life is so busy, you need to make time for you, and make sure […]

Saving for a house? Here’s 3 things you can do today!

Saving for a house during a cost of living crisis? There’s 3 things you can do today to help you on your way: 1. Open a LISA An absolute no brainer if you’re saving for your first home. But what is it? A Lifetime ISA (LISA) is a house or pension savings account that you […]

How to budget on a low income

How to budget on a low income Times are hard for many of us right now, but especially for those living on a low income and battling the cost of living crisis. With the rate of inflation increasing ahead of the rate of pay growth, it’s never been a more crucial time to budget and […]

Download the Financielle app now Never be overwhelmed by money again.